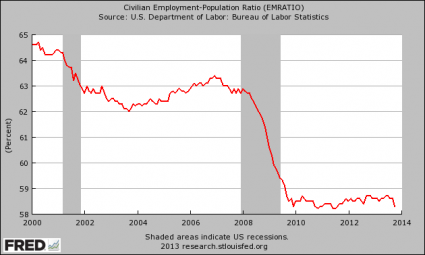

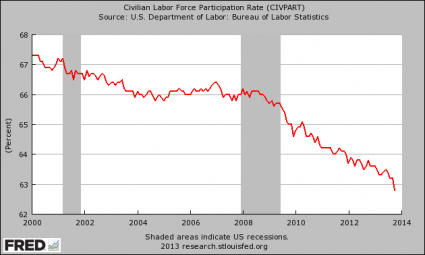

Americans’ Participation in Labor Force Hits 35-Year Low - CNSnews - November 12, 2013 - The percentage of American civilians 16 or older who have a job or are actively seeking one dropped to a 35-year low in October, according to the Bureau of Labor Statistics.

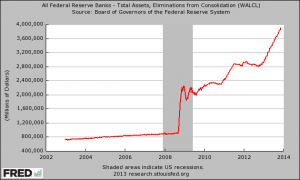

The Federal Reserve Is Monetizing A Staggering Amount Of U.S. Government Debt - The Economic Collapse Blog - Michael Snyder - November 14th, 2013 - The Federal Reserve is creating hundreds of billions of dollars out of thin air and using that money to buy U.S. government debt and mortgage-backed securities and take them out of circulation. Since the middle of 2008, these purchases have caused the Fed's balance sheet to balloon from under a trillion dollars to nearly four trillion dollars. This represents the greatest central bank intervention in the history of the planet, and Janet Yellen says that she does not anticipate that it will end any time soon because "the recovery is still fragile". Of course, as I showed the other day, the truth is that quantitative easing has done essentially nothing for the average person on the street. But what QE has done is that it has sent stocks soaring to record highs. Unfortunately, this stock market bubble is completely and totally divorced from economic reality, and when the easy money is taken away the bubble will collapse. Just look at what happened a few months ago when Ben Bernanke suggested that the Fed may begin to "taper" the amount of quantitative easing that it was doing. The mere suggestion that the flow of easy money would start to slow down a little bit was enough to send the market into deep convulsions. This is why the Federal Reserve cannot stop monetizing debt. The moment the Fed stops, it could throw our financial markets into a crisis even worse than what we saw back in 2008.

The problems that plagued our financial system back in 2008 have never been fixed. They have just been papered over temporarily by trillions of easy dollars from the Federal Reserve. All of this easy money is keeping stocks artificially high and interest rates artificially low. Right now, the Federal Reserve is buying approximately 85 billion dollars worth of U.S. government debt and mortgage-backed securities each month. We are told that the portion going to buy U.S. government debt each month is approximately 45 billion dollars, but who knows what the Fed is actually doing behind the scenes. In any event, by creating money out of thin air and using it to remove U.S. Treasury securities out of circulation, the Federal Reserve is essentially monetizing U.S. government debt at a staggering rate. But Federal Reserve officials continue to repeatedly deny that what they are doing is monetizing debt. For instance, Federal Reserve Bank of Atlanta President Dennis Lockhart strongly denied this back in April: "I object to the view that the Fed is monetizing the debt". How in the world can Fed officials possibly deny that they are monetizing the debt? Well, because the Fed is promising that it is going to eventually sell back all of the securities that it is currently buying. Since the Fed does not plan to keep all of this government debt on its balance sheet indefinitely, that means that they are not actually monetizing it according to their twisted logic.

Federal Reserve Whistleblower Tells America The REAL Reason For Quantitative Easing - The Economic Collapse Blog - Michael Snyder, on November 12th, 2013

Spot The Striking Similarity - Zero Hedge - Tyler Durden November 16, 2013

As young people hunker down, homeownership dips - CBS Moneywatch - Erik Sherman - November 15, 2013 - Americans are changing their housing habits in ways that could affect the U.S. economy. Younger people are becoming less mobile and are less inclined to buy a place to live, while broader homeownership numbers are down, according to recent data from the U.S. Census Bureau. An Associated Press analysis found that percentage of young adults who move to a new locale has hit a 50-year low. Only just over 23 percent of people ages 25 to 29 moved in the past year, down from roughly 25 percent the previous year and the lowest figure since 1963. Why are younger adults passing on buying a home? Likely because the weak job market, stagnant wages and high levels of college loan debt are keeping them in existing apartments with roommates or living with their parents. The homeownership rate between 2010 and 2012 was nearly 65 percent, a 1.7 percent decline from the 2007 to 2009 period, according to the Census Bureau. It is difficult to tell how much of the drop is due to young adults not purchasing homes or to other factors. The time range coincided with the economic recession, a rash of property foreclosures that followed the housing crash and a significant tightening of credit. All three factors likely contributed to people being unable to afford homes or to losing the homes that they already had. Another finding in the Census Bureau analysis was that the median home value in the U.S. decreased between 2007 and 2012. What is surprising is that some areas weathered the decline, and a few even saw an increase in medium home values: 28 states saw a decline in median home value, but 19 states actually experienced an increase.

Why hardly anyone signed up for Obamacare - Hint: It has nothing to do with tech glitches at HealthCare.gov - Marketwatch - Jonnelle Marte - November 17, 2013 - It may seem surprising that just 106,000 Americans managed to enroll in Obamacare, choosing a health plan through the new state or federally run insurance exchanges. That is, until one considers human nature. Though the enrollment is about 1.5% of the 7 million people expected to buy coverage through the exchanges next year, and well below expectations for the first month, experts say there’s reason to think our procrastination may be as much to blame as bad programming. People typically approach healthcare open enrollment in waves, with a burst of people, usually about 15% of participants, signing up at the start of the enrollment period and then a huge rush of purchases happening toward the end of the period, says Tony DeNucci, a managing director with Towers Watson, a professional services company. “There are people who aren’t paying attention and don’t want to deal with it until the last minute,” says DeNucci. The type of person who enrolls in next year’s insurance plan six weeks in advance is also the type of person who files their tax return in January. About 22% of people make insurance decisions in the last two days of open enrollment periods, health officials said during a media call Wednesday. Kathleen Sebelius, secretary of Health and Human Services, also attributed some of the delay to the idea that consumers often take their time making health insurance decisions. “Insurance is very different than buying a toaster,” Sebelius said during the call. “As more people shop and talk things over with their families we expect these numbers to rise.” ALSO SEE: Should you keep your health insurance plan?

Even people who signed up for insurance on Oct.1—to the extent that they were able to given technical setbacks on HealthCare.gov and some of the state-run exchanges—won’t be covered until Jan. 1, and won’t have a premium payment until roughly Dec. 15. It wouldn’t be surprising, financial experts say, if many people were waiting to get closer to that moment of gratification to take action. “People are often reactive rather than proactive,” says Taylor Gang, a principal at Evensky & Katz, a wealth management firm based in Coral Gables, Fla.

Obamacare rollout: Doctors concerned about patients, care, fees - CBS News - Wyatt Andrews - November 11, 2013

No comments:

Post a Comment